In

part 1 we looked at some examples of what happens when the audience can no longer suspend its disbelief in a currency.

What was the magic? The magic was the magnificent illusion that money printing increased wealth. It certainly looked that way, despite all the common-sense interpretation that would have you believe that it doesn't. But that's the beauty of a wonderfully performed magic trick. Something impossible seems to happen. You know it can't happen, but it looks like it did, and what's the harm in letting yourself believe?

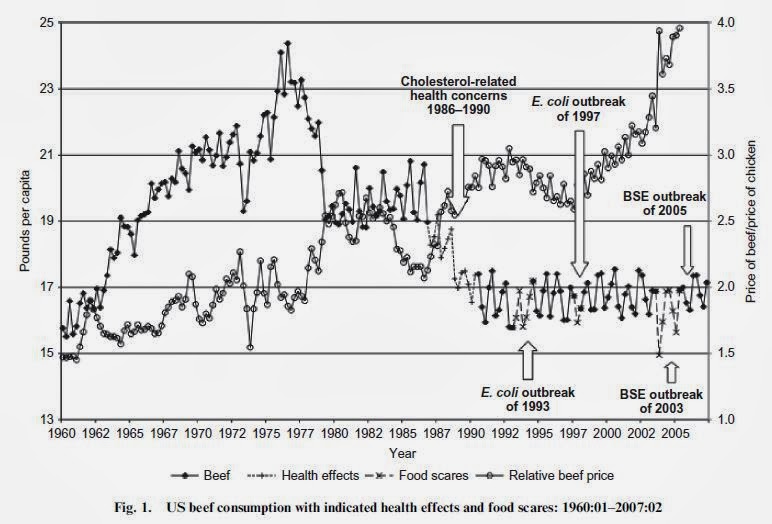

The latest round of the great trick really began in the late 1950s. Spending by the US government increased the demand for labour by the millions, which allowed women to enter the workforce in large numbers.

The main uptick in the labour force participation rate began in the early '60s, but the real bottom (on this graph) was in the mid '50s. One obvious source of stimulus in the 1960s would have been the Vietnam War, on which the US gov't spent the equivalent of

$738 billion, in 2011 dollars (pdf). That kind of money created a lot of jobs--mainly in the military industries, but also for lobbyists.

At the same time, the

"Great Society" was in full swing. Lots of public works projects. The same thing happened up here in Canada, with a huge increase in universities, highways, and transit systems. All this spending created a lot of jobs. Nobody asked whether these jobs were really necessary. Would the public works projects pay off?

Certainly they appeared to make society more prosperous. But was it real prosperity or just a magic trick? Was it an illusion, or something more sinister . . .

A thief and a magician enter a convenience store. The thief says to the magician, "Watch this", and promptly places three chocolate bars into his pocket so smoothly that nobody else notices. He is just about to leave when the magician calls him back and says, "I've got a better trick." The magician approaches the shopkeeper, and asks if he'd like to see a trick. "I can make three chocolate bars disappear and reappear." He unwraps three chocolate bars and eats them. When the shopkeeper asks to see them reappear, the magician points to the thief and says, "They are in my friend's pocket."

In the earliest part of my education I recall, we were fed the belief that it was right for women to enter the workforce, and it followed that once women wanted to work, all these jobs opened up for them. Millions of them.

Why can't it happen now?

Look at the unemployed--the real unemployed. Their numbers are reflected in a massive increase in

duration of unemployment not to mention the increase in the reported unemployment rate.

I thought the unemployment rate was supposed to drop when interest

rates were low. Data from BLS.

Don't the unemployed want jobs? Why don't jobs magically appear for them like they did in the 60s?

Impressive job creation from the 1960s until about 2000.

It stalled briefly during the Volcker high-interest-rate period

of the early 80s. Data from BLS.

The trouble is similar to what our magician friend in the story above might face if the shopkeeper suddenly demanded a repeat performance, this time with meat pies. The magician can only perform a trick like that so many times. Perhaps he becomes too engorged with chocolate bars and meat pies. Perhaps there aren't any that can "appear" in his friend's pocket. Or maybe the shopkeeper simply won't be fooled any more.

That's funny. All that money of yours that disappeared was

supposed to reappear in my hand. Errrm, sorry?

At least is isn't as bad as Siegfried and Roy's last trick with the tiger.

What does the rest of the world think?

Too lazy to update this. Sorry. To mid 2011. But I doubt it's gotten better.

It looks like the rest of the world started to lose faith in the US dollar in the '90s. Remember the Strong Dollar Policy under Clinton? Looks like somebody thought it was a selling opportunity.

But the problems with the money-creating approach became apparent by 1970. Nixon kept the system going a bit longer with his trick of taking the dollar off the gold standard, so the US would not have to exhaust its stored gold redeeming green coupons. The system ran out of gas again at the end of the 70s, but Volcker's trick of raising interest rates gave the US 20+ years of slowly falling interest rates, which allowed the audience to keep believing the illusion.

But even then, it should have been clear that something was up. GDP as it was defined at the time was climbing, but some of its ancillaries were not keeping up.

Data from Handselbanken Capital Markets.

It is

difficult to imagine just how the economy grows without similar increases in the use of copper and zinc, both of which are tough to replace. One comment wondered if we replaced copper and zinc with plastics. Some piping maybe. But not much wiring.

As

I proposed earlier, what really happened in the late 1970s was a contraction in the economy, which was hidden by fudging reported GDP. If real GDP is tied to demand for copper and zinc, then I would say that (from the above chart) world GDP was overstated by approximately 80% as of 2005. It's hard to imagine that that number has gotten smaller subsequently. Either that, or the "value" of lawyers bills, lobby groups, US medical expenses, overspending on military wonder weapons, financial charges and skimming, and other less than productive enterprises now constitutes just under 50% of the world "economy". I hope it makes you feel rich.

With lower demand came lower exploration expenditures--at least for base metals.

I think this graph shows the change in mindset from the past to the present. Don't mine base metals; mine money (gold). And this established the precedent for today's industrial ideal:

don't make products, make money. And so the business model changed: from producing real products, which improved lives and increased the wealth of everyone; to making money through methods including outsourcing and speculation, which improved the lives and wealth of only a few.

Back to jobs.

After the little scare in 1980, we had 20 years of lower interest rates, during which the US labour force participation rate increased to its highest level in history. After the internet bubble popped, the US Fed shoved interest rates down, igniting a nice housing bubble, which created a lot of construction, real estate, and retail jobs. Unfortunately, these only matched the losses of manufacturing jobs--until about 2007. More recently, the number of full-time jobs is falling.

The magician has pulled all the rabbits there are out of the hat.

If money printing can't create jobs anymore, the pain that is to come will dwarf the pain already felt. The labour force participation rate will fall to the level of the 1950s unless there is another rabbit in there somewhere.

Too bad they'll all be low-paying jobs.