The topic of national suicide seems an appropriate topic for the anniversary of the Japanese attack on Pearl Harbour. The Japanese people bore very little animosity to America. No doubt many of them remembered the aid that came to Japan after the big earthquake in 1923. Sadly, like in all other countries, the Japanese people were not in control of their country.

Like all wars, this war was sold to the people as a matter of national survival. But it was to be a survival in which Japanese people were destroyed in vast numbers to "save the nation." By the end of the war, soldiers were being outright sacrificed in order to achieve limited tactical successes.

The movie For Those We Love*, the pilots are preparing to leave on their final mission. The father, brother, and sister of one of the pilots have arrived to see him off. As he is about to enter his plane, his father pleads for him to come back to talk to him one last time (it's at about 2:35 of the following video). Unfortunately, his last words for his son are a lame cliche ("Do your best. We are all counting on you." And so on). My thought was that if that were my son about to fly off to die, I would have told him, "See that tent over there? That's where your commanding officers will all go as you leave. So after you take off, come back and strafe the hell out of it."

Now I read in this article that at least one pilot did attack his commanding officers. The article argued that the Kamikaze phenomenon in the latter part of the Pacific War was a particularly noxious brew of statism and Zen Buddhism.

I don't believe the Zen Buddhism part to have been necessary. The kamikaze pilots were not driven to suicide out of a philosophical concept of nothingness. They were ordered to, or perhaps pressured ("Come on, you don't want Japan to lose the war because of you, do you?"). The desire for death came down from the top, mostly from people who did not have the grace to kill themselves afterward.

The noxious mix came from a government that equated "the country" with themselves rather than with the people. As a consequence, the government was willing to sacrifice as many of its own people as was necessary to ensure its own survival. The lesson here applies not only to the hapless wartime Japanese, but to everyone in the world from the United States and Japan, to the Ukraine, and even non-state actors such as ISIL. The most obvious antecedents are in the suicide bombers that have struck targets around the world.

Today most of the developed countries of the world are pursuing economic policies "to save the nation". Unfortunately, they are predicated on arguments that the elderly will bankrupt the state: thus the state must strike back through low interest rates and understating inflation.

I like that choice of words: "merely reduce the growth of future benefits". Those future benefits were to compensate for rising prices which are themselves a function of the activities of the state. The remedy, that the elderly can eat chicken when the price of beef goes up; then cat food when the price of chicken rises, is a recipe for poverty. Unfortunately, starving the elderly is necessary to save the "nation".

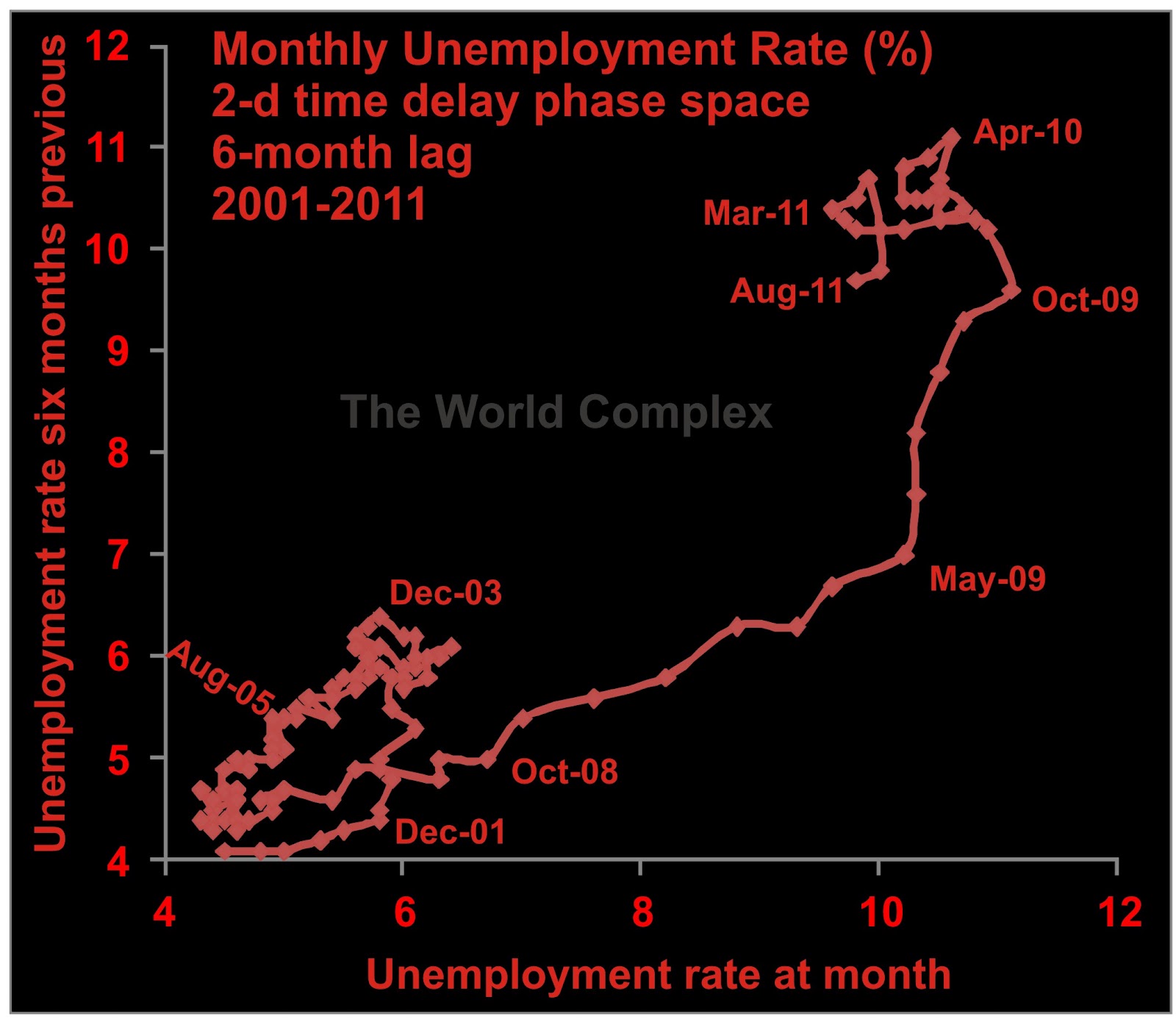

I have argued that the low-interest-rate policy has harmed employment by reducing the costs of losses in financial speculation relative to productive investment. Thus, starving white and blue-collar workers of all ages is also necessary to save the "nation".

The massive size of the debts accumulated across the developed world will be borne by our children, encouraging a lower standard of living for them. Thus, starving children is also necessary to "save the nation".

In WW2, Japan sent its young men off to die trying to sink American ships. Now governments all around the world are casting off their citizens, stealing their lives a bit at a time to push the day of their own reckoning a little further into the distance. The only difference is they are not yet ordering us to die.

* I have to advise you that this is not a very good film.

Like all wars, this war was sold to the people as a matter of national survival. But it was to be a survival in which Japanese people were destroyed in vast numbers to "save the nation." By the end of the war, soldiers were being outright sacrificed in order to achieve limited tactical successes.

The movie For Those We Love*, the pilots are preparing to leave on their final mission. The father, brother, and sister of one of the pilots have arrived to see him off. As he is about to enter his plane, his father pleads for him to come back to talk to him one last time (it's at about 2:35 of the following video). Unfortunately, his last words for his son are a lame cliche ("Do your best. We are all counting on you." And so on). My thought was that if that were my son about to fly off to die, I would have told him, "See that tent over there? That's where your commanding officers will all go as you leave. So after you take off, come back and strafe the hell out of it."

Now I read in this article that at least one pilot did attack his commanding officers. The article argued that the Kamikaze phenomenon in the latter part of the Pacific War was a particularly noxious brew of statism and Zen Buddhism.

I don't believe the Zen Buddhism part to have been necessary. The kamikaze pilots were not driven to suicide out of a philosophical concept of nothingness. They were ordered to, or perhaps pressured ("Come on, you don't want Japan to lose the war because of you, do you?"). The desire for death came down from the top, mostly from people who did not have the grace to kill themselves afterward.

The noxious mix came from a government that equated "the country" with themselves rather than with the people. As a consequence, the government was willing to sacrifice as many of its own people as was necessary to ensure its own survival. The lesson here applies not only to the hapless wartime Japanese, but to everyone in the world from the United States and Japan, to the Ukraine, and even non-state actors such as ISIL. The most obvious antecedents are in the suicide bombers that have struck targets around the world.

Today most of the developed countries of the world are pursuing economic policies "to save the nation". Unfortunately, they are predicated on arguments that the elderly will bankrupt the state: thus the state must strike back through low interest rates and understating inflation.

In fact, President Barack Obama’s budget wouldn’t take a dime from anyone’s current Social Security check. It would merely reduce the growth of future benefits by changing the way the government calculates inflation.What the president has done is to endorse the notion that our current Consumer Price Index overstates inflation, because it doesn’t account for people’s ability to switch to lower-cost goods. If the price of beef goes up, people eat more chicken.

I like that choice of words: "merely reduce the growth of future benefits". Those future benefits were to compensate for rising prices which are themselves a function of the activities of the state. The remedy, that the elderly can eat chicken when the price of beef goes up; then cat food when the price of chicken rises, is a recipe for poverty. Unfortunately, starving the elderly is necessary to save the "nation".

I have argued that the low-interest-rate policy has harmed employment by reducing the costs of losses in financial speculation relative to productive investment. Thus, starving white and blue-collar workers of all ages is also necessary to save the "nation".

The massive size of the debts accumulated across the developed world will be borne by our children, encouraging a lower standard of living for them. Thus, starving children is also necessary to "save the nation".

In WW2, Japan sent its young men off to die trying to sink American ships. Now governments all around the world are casting off their citizens, stealing their lives a bit at a time to push the day of their own reckoning a little further into the distance. The only difference is they are not yet ordering us to die.

* I have to advise you that this is not a very good film.