There are many opinions about the value of gold in the ground, some of which have changed through time.

As people become more familiar with the NI 43-101 regulations, investors have come to distinguish between resources, proven reserves, and measured and indicated ounces. As a consequence, company prices no longer react much to raw results; investors now wait to see the result of a formal technical report to see if more ounces are discovered or upgraded to proven reserves.

The value of gold and the ground will depend on the price of gold. For some of the examples above, the value of proven and probable reserves was set at about one-quarter to one-fifth of the spot gold price. Other authors place a lower value on such gold.

There is a problem with the model for gold exploration. There does not appear to be enough money in it to make it worthwhile.

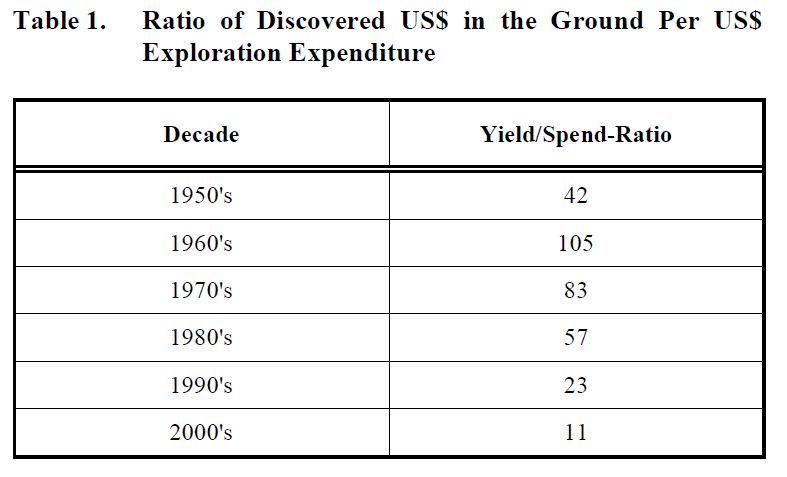

In the face of a rising price of gold, the payback on gold exploration appears to have fallen alarmingly. The idea that an exploration company's price will rise tenfold on a discovery may have been valid forty years ago, but with the level of success indicated on the above table, such a payback would leave nothing for the poor developer of the eventual mine.

It is possible to infer from this chart that we are running out of gold to discover. Here at the World Complex, our view is that a significant factor in this decline is the increased level of regulatory complexity a company must navigate in order to officially "discover" an amount of gold. In particular, the amount of drilling required to define one million ounces of gold is much greater at present than was the case in, say, 1960.

Ultimately, the extra money is not wasted. The additional definition of the resource may not have been necessary to "prove" the deposit in years past--but it would have been done to define the reserve during the planning stages of the mine. So the effect of recent regulation has been to shift some of the spending burden from the mine developers to the junior explorers.

In effect, the increase in cost defining resources is mitigated somewhat in the development phase. In principal, it should cost slightly less to develop a mine after the definition of the mineral reserve than would have been the case in the distant past, suggesting a net benefit to developers and producers. I have not pulled together enough data to study whether the share price of producers has improved with respect to typical metrics (reserves or production) to see if this shift can be separated from the impact in the rising price of gold.

It may be that there is another revaluation to come for mining companies.

As people become more familiar with the NI 43-101 regulations, investors have come to distinguish between resources, proven reserves, and measured and indicated ounces. As a consequence, company prices no longer react much to raw results; investors now wait to see the result of a formal technical report to see if more ounces are discovered or upgraded to proven reserves.

The value of gold and the ground will depend on the price of gold. For some of the examples above, the value of proven and probable reserves was set at about one-quarter to one-fifth of the spot gold price. Other authors place a lower value on such gold.

There is a problem with the model for gold exploration. There does not appear to be enough money in it to make it worthwhile.

Value of gold discovered per dollar of exploration through time.

In the face of a rising price of gold, the payback on gold exploration appears to have fallen alarmingly. The idea that an exploration company's price will rise tenfold on a discovery may have been valid forty years ago, but with the level of success indicated on the above table, such a payback would leave nothing for the poor developer of the eventual mine.

It is possible to infer from this chart that we are running out of gold to discover. Here at the World Complex, our view is that a significant factor in this decline is the increased level of regulatory complexity a company must navigate in order to officially "discover" an amount of gold. In particular, the amount of drilling required to define one million ounces of gold is much greater at present than was the case in, say, 1960.

Ultimately, the extra money is not wasted. The additional definition of the resource may not have been necessary to "prove" the deposit in years past--but it would have been done to define the reserve during the planning stages of the mine. So the effect of recent regulation has been to shift some of the spending burden from the mine developers to the junior explorers.

In effect, the increase in cost defining resources is mitigated somewhat in the development phase. In principal, it should cost slightly less to develop a mine after the definition of the mineral reserve than would have been the case in the distant past, suggesting a net benefit to developers and producers. I have not pulled together enough data to study whether the share price of producers has improved with respect to typical metrics (reserves or production) to see if this shift can be separated from the impact in the rising price of gold.

It may be that there is another revaluation to come for mining companies.