As you contemplate your portfolios this tax-loss season . . .

Dust flux, Vostok ice core

Two dimensional phase space reconstruction of dust flux from the Vostok core over the period 186-4 ka using the time derivative method. Dust flux on the x-axis, rate of change is on the y-axis. From Gipp (2001).

Showing posts with label look out below. Show all posts

Showing posts with label look out below. Show all posts

Tuesday, December 17, 2013

Sunday, May 5, 2013

Break in generational employment trend

It's been awhile since we last revisited unemployment. I have largely abandoned its study because of the distortions that have been built into its present calculation. These distortions become clear in looking at the labor force participation rate, which is the proportion of the adult population engaged in full time employment, and which is readily available at the Bureau of Labor Statistics.

The website gives you monthly data going back to 1948.

Available data are monthly, but I have only used the year-end numbers in the above graph.

The profile of employment across the United States was no doubt greatly different in 1948 than at present. In 1948 it was a lot less common to see both parents fully employed than was the case in 2000. Assuming that all families have at least one parent working full time, the peak value of about 67% in the late 1990s would suggest that 34% of families had two full-time working parents. Part-time workers are not counted in this statistic, and no doubt they were many.

The increase in participation from the early 1960s to the late 1990s reflects a major change in the structure of employment over the past two generations, with more married women entering the workforce.

In the lagged phase space we see two areas of attraction--the first in the 59% participation, and the second more recently, around 67%. We also note that the system has recently moved out of the higher area of attraction. The relative number of fully employed people is falling. How low can it go?

Below we see a topologically equivalent phase space constructed using the time-derivative method--plotting the participation rate against its rate of change, averaged over four years.

The same two areas of attraction appear, with what might be a third at around 64%. The current trajectory looks like it is heading there--so it doesn't appear that labor force participation will shrink much going forward.

Labor force participation increased during the period of falling interest rates after Volcker raised them so high in 1980. Their subsequent drop ignited a stock market bubble, which finally popped in the year 2000. The participation rate appeared to be heading lower--but intervention in interest rates inflated a bubble in real estate prices, "creating" lots of jobs in sales and construction--until it, too popped.

Based on the above graph, it looks as though most of the damage to employment of the bubble popping is over . . . unless . . .

Unless there is another bubble which we haven't considered. One that has been inflating since the early 1960s. One built on expansion of credit which has funded wars and expanded the economy to accommodate influxes of workers from family farms and young women wanting to take control of their own affairs.

Is this really logical? Did millions of jobs suddenly appear because there was this generation of young women who wanted to work?

One of the key features of a bubble is a story--a story that justifies the expansion, and which tells you that this time the expansion is not the inflation of a bubble. It looks to me that the happy story of women entering the workforce may be such a story--and there are still many millions more to leave the full-time labor force.

The website gives you monthly data going back to 1948.

Available data are monthly, but I have only used the year-end numbers in the above graph.

The profile of employment across the United States was no doubt greatly different in 1948 than at present. In 1948 it was a lot less common to see both parents fully employed than was the case in 2000. Assuming that all families have at least one parent working full time, the peak value of about 67% in the late 1990s would suggest that 34% of families had two full-time working parents. Part-time workers are not counted in this statistic, and no doubt they were many.

The increase in participation from the early 1960s to the late 1990s reflects a major change in the structure of employment over the past two generations, with more married women entering the workforce.

In the lagged phase space we see two areas of attraction--the first in the 59% participation, and the second more recently, around 67%. We also note that the system has recently moved out of the higher area of attraction. The relative number of fully employed people is falling. How low can it go?

Below we see a topologically equivalent phase space constructed using the time-derivative method--plotting the participation rate against its rate of change, averaged over four years.

The same two areas of attraction appear, with what might be a third at around 64%. The current trajectory looks like it is heading there--so it doesn't appear that labor force participation will shrink much going forward.

Labor force participation increased during the period of falling interest rates after Volcker raised them so high in 1980. Their subsequent drop ignited a stock market bubble, which finally popped in the year 2000. The participation rate appeared to be heading lower--but intervention in interest rates inflated a bubble in real estate prices, "creating" lots of jobs in sales and construction--until it, too popped.

Based on the above graph, it looks as though most of the damage to employment of the bubble popping is over . . . unless . . .

Unless there is another bubble which we haven't considered. One that has been inflating since the early 1960s. One built on expansion of credit which has funded wars and expanded the economy to accommodate influxes of workers from family farms and young women wanting to take control of their own affairs.

Is this really logical? Did millions of jobs suddenly appear because there was this generation of young women who wanted to work?

One of the key features of a bubble is a story--a story that justifies the expansion, and which tells you that this time the expansion is not the inflation of a bubble. It looks to me that the happy story of women entering the workforce may be such a story--and there are still many millions more to leave the full-time labor force.

Wednesday, April 24, 2013

Gold-silver ratio in phase space

The reconstructed phase space portrait is one tool that can be used to gain insight into the dynamics of complex systems, whether these systems be natural or man-made.

Today we will use these tools to look at precious metals.

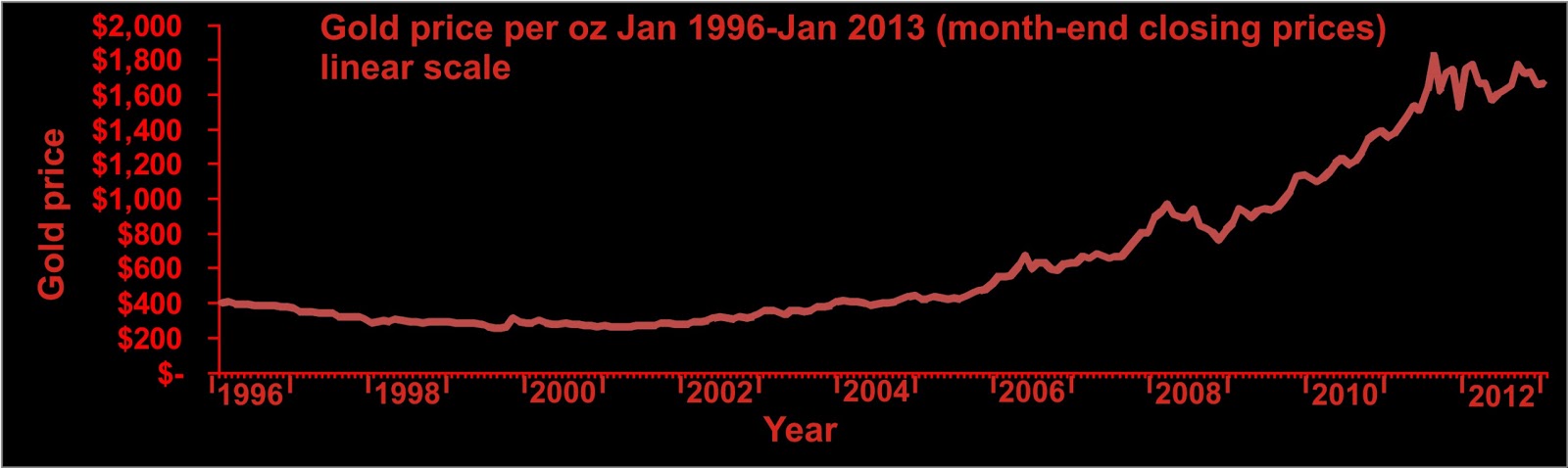

The near-constant slope over long stretches of this plot tells us that gold is already increasing in price exponentially. So don't say that gold price will increase exponentially during a financial crisis. It is already doing so, and has been since early 2001 (notwithstanding the recent turmoil).

The break in slope in late 2005 tells us that the gold price suddenly began to increase more rapidly. I don't know if anything unusual happened in late 2005, but there was a bland warning by the ECB issued in December 2005 about growing global financial imbalances.

Reconstructing phase space portraits normally requires two or more time series, sampled at equivalent intervals. You can simply plot one series against the other (a scatter plot). If you are using excel or a similar program, this is remarkably easy.

Looks impressive--the gold line represents a gold:silver ratio of about 60. Deviations from that line represent deviations in this ratio. Silver's rise to nearly $50 in 2011 causes the funny looking nose on the graph at upper right. The curve represents the time evolution of the system, which moved in herky-jerky fashion from the lower left (in January 2000) towards the upper right of the graph (a little while ago). Each plotted point represents the state at the end of each month until roughly the present.

For graphs covering at least an order of magnitude, it may be worth using logarithmic axes.

The problem with these graphs is the presence of the US dollar. Most of the action in the plot is due to the declining value of the US dollar. To remove it, let us consider only the gold:silver ratio itself.

There are a number of long-accepted methods for projecting a single data series into a state space of more than one dimension. The intuitively obvious approach is to plot the data against its first (and higher, if desired) time derivatives. The approach I have used most commonly in these pages is a time delay plot, in which the respective observations are plotted against another, older observation. The lag is the number of time steps between the two observations, and there are prescribed methods for establishing an ideal lag.

Taking the month-end ratio of the gold price to the silver price, plotting it against a lagged copy of itself (delayed by one year), we see the following.

We are presently near where we started (just before the last financial crisis, and currently following a trajectory similar to that which we followed in the summer of 2008 (the yellow dot represents where we would be if April ends at today's prices). Given what we've recently experienced in the metals markets and stocks, it is extremely worrisome to consider we are only at the equivalent of mid-summer 2008!

There is more to the story--plotting phase space in only two dimensions can be a little risky because the third dimension may convey a lot of information. To create the third dimension, we apply a second lag equal to the first--so that the third axis represents an observation two lag periods behind the observation plotted on the first axis.

In the above graph, the red curve represents the 2-d projection shown above plotted on a reference plane (z=55)--and the green curve represents the 3-dimensional phase space portrait shown relative to the reference. Where there are green dashed lines between the 3-d and 2-d plots, the 3-d plot is above the reference plane, and where there are red dashed lines, the 3-d plot lies below the reference plane.

In the 3-d plot, we see that the current trajectory (near the bottom of the graph) is quite a bit below the trajectory during the crisis of 2008. It may be that the 2008 financial crisis was one of financial institution solvency, whereas our current crisis is starting to look like one of financial system failure. If this is the explanation for the differing trajectories then my projection is that we are going to see something we haven't seen before.

The gold-silver ratio has the potential to rise to heights never before seen. The reason is that major crises encourage hoarding and flight; and it is much easier to flee with a million dollars in gold than a million dollars in silver.

Today we will use these tools to look at precious metals.

The near-constant slope over long stretches of this plot tells us that gold is already increasing in price exponentially. So don't say that gold price will increase exponentially during a financial crisis. It is already doing so, and has been since early 2001 (notwithstanding the recent turmoil).

The break in slope in late 2005 tells us that the gold price suddenly began to increase more rapidly. I don't know if anything unusual happened in late 2005, but there was a bland warning by the ECB issued in December 2005 about growing global financial imbalances.

Reconstructing phase space portraits normally requires two or more time series, sampled at equivalent intervals. You can simply plot one series against the other (a scatter plot). If you are using excel or a similar program, this is remarkably easy.

Looks impressive--the gold line represents a gold:silver ratio of about 60. Deviations from that line represent deviations in this ratio. Silver's rise to nearly $50 in 2011 causes the funny looking nose on the graph at upper right. The curve represents the time evolution of the system, which moved in herky-jerky fashion from the lower left (in January 2000) towards the upper right of the graph (a little while ago). Each plotted point represents the state at the end of each month until roughly the present.

For graphs covering at least an order of magnitude, it may be worth using logarithmic axes.

The problem with these graphs is the presence of the US dollar. Most of the action in the plot is due to the declining value of the US dollar. To remove it, let us consider only the gold:silver ratio itself.

There are a number of long-accepted methods for projecting a single data series into a state space of more than one dimension. The intuitively obvious approach is to plot the data against its first (and higher, if desired) time derivatives. The approach I have used most commonly in these pages is a time delay plot, in which the respective observations are plotted against another, older observation. The lag is the number of time steps between the two observations, and there are prescribed methods for establishing an ideal lag.

Taking the month-end ratio of the gold price to the silver price, plotting it against a lagged copy of itself (delayed by one year), we see the following.

We are presently near where we started (just before the last financial crisis, and currently following a trajectory similar to that which we followed in the summer of 2008 (the yellow dot represents where we would be if April ends at today's prices). Given what we've recently experienced in the metals markets and stocks, it is extremely worrisome to consider we are only at the equivalent of mid-summer 2008!

There is more to the story--plotting phase space in only two dimensions can be a little risky because the third dimension may convey a lot of information. To create the third dimension, we apply a second lag equal to the first--so that the third axis represents an observation two lag periods behind the observation plotted on the first axis.

In the above graph, the red curve represents the 2-d projection shown above plotted on a reference plane (z=55)--and the green curve represents the 3-dimensional phase space portrait shown relative to the reference. Where there are green dashed lines between the 3-d and 2-d plots, the 3-d plot is above the reference plane, and where there are red dashed lines, the 3-d plot lies below the reference plane.

In the 3-d plot, we see that the current trajectory (near the bottom of the graph) is quite a bit below the trajectory during the crisis of 2008. It may be that the 2008 financial crisis was one of financial institution solvency, whereas our current crisis is starting to look like one of financial system failure. If this is the explanation for the differing trajectories then my projection is that we are going to see something we haven't seen before.

The gold-silver ratio has the potential to rise to heights never before seen. The reason is that major crises encourage hoarding and flight; and it is much easier to flee with a million dollars in gold than a million dollars in silver.

Subscribe to:

Posts (Atom)